Blog

May 6, 2026

Filip M. Rams, Michael G. Nicolella

Investment funds, tax advisors, decentralized finance projects, and the fifteen percent of Americans who own cryptocurrency should pay close attention to the proposed bill “Digital Asset Market Clarity Act,” known as the CLARITY Act. Here is what this post covers:

On April 8, 2026, Treasury Secretary Scott Bessent published an op-ed in the Wall Street Journal calling on the Senate to quickly pass the CLARITY Act. His message was simple: “A growing share of crypto development relocated to places with clear rules. The benefits of domiciling in the U.S. rarely outweighed the risks.” Scott Bessent, The Wall Street Journal, April 8, 2026.

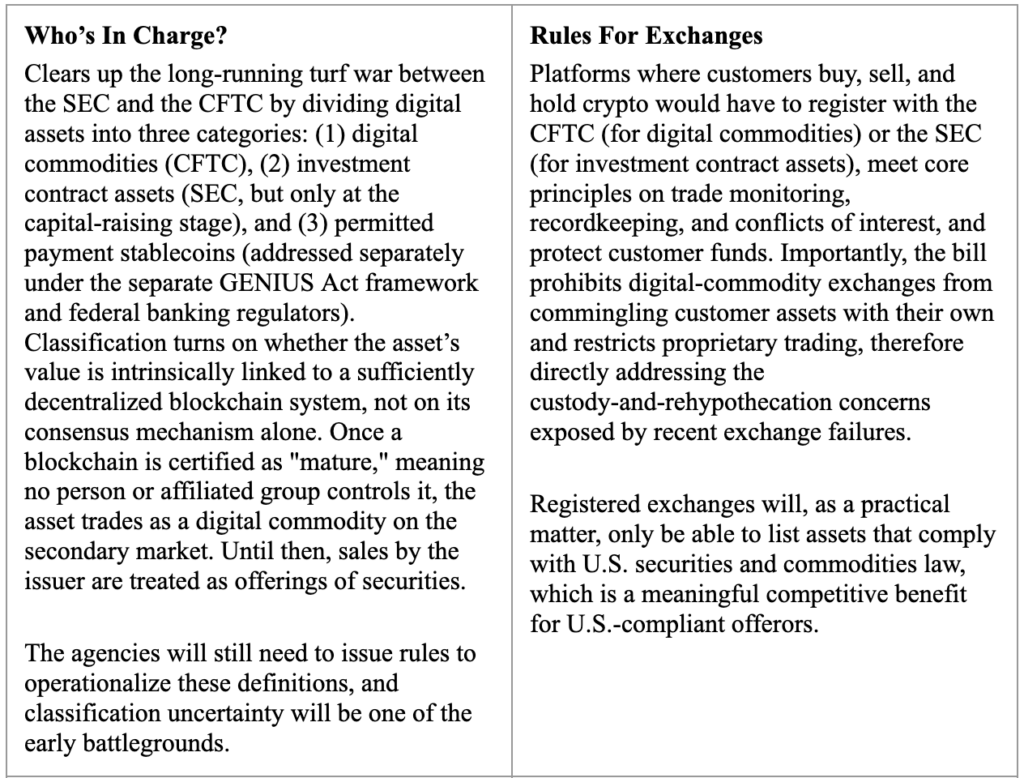

The central legal issue the CLARITY Act tries to resolve is straightforward: which digital-asset activity should be regulated as a public offering or public exchange of a security or commodity, and which should be unregulated as private, peer-to-peer activity?

The bill draws that line in three places: (1) how digital assets are classified (commodity vs. security); (2) how exchanges and brokers are registered; and (3) what is carved out for decentralized finance and peer-to-peer transactions. Additional questions worth asking are: who gains from where those lines fall? U.S.-domiciled offerors and registered exchanges that will enjoy a compliant, predictable market. And who may lose? Retail purchasers on the DeFi side of the line, where the traditional investor-protection rationale for regulation still applies but the statutory regime may not.

The CLARITY Act is a proposed rulebook for the public side of the U.S. digital-asset market covering initial coin offerings, registered exchanges, and the brokers and dealers operating on those exchanges. It leaves decentralized, peer-to-peer activity largely outside that perimeter. The core mechanics are following:

The bill was introduced in May 2025 and cleared the House in July 2025 by a 294–134 vote. That was the easy part. Two Senate committees, Banking and Agriculture, are each marking up their own version covering different pieces of the market. Both must be finalized, merged, and then reconciled with the House version. That is a lot of moving pieces, and the window is narrowing: if the Senate does not act before midterm-election campaigns pick up this summer, the bill risks losing momentum entirely. Two fights are causing this delay.

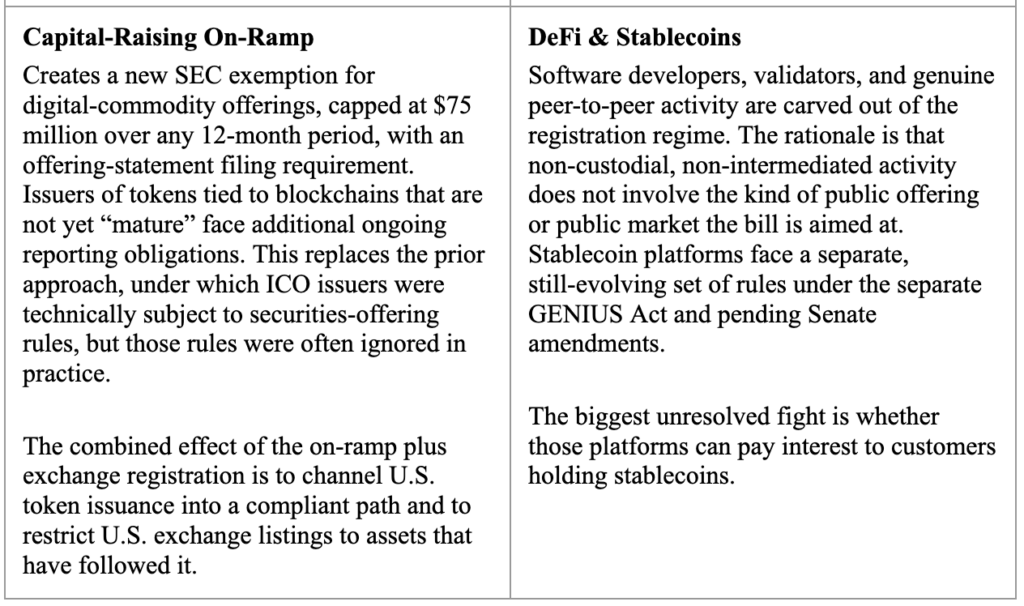

The first is stablecoin interest and whether platforms can pay holders a yield on stablecoin balances. Banks say no, because interest-bearing stablecoins compete directly with insured deposits. Crypto firms say yes, because yield is central to the product. Coinbase, the largest U.S.-based cryptocurrency exchange, withdrew its support for the bill over this issue earlier this year.

The second is the scope of the DeFi carve-out. The bill’s rationale for exempting decentralized, peer-to-peer activity is conceptually sound because it is not a public offering or a public exchange. But the classical securities-law exemptions for private transactions rest on knowing the purchaser’s sophistication, relationship to the issuer, or accredited status. DeFi counterparties are anonymous. That mismatch is likely to create a loophole that sophisticated projects will structure into, and that will expose less sophisticated retail purchasers to risks the regulated structure was designed to prevent.

In the short term, nothing changes. The bill has not passed. But the practical implications are close enough that holders and practitioners should be positioning now rather than reacting later. The items below combine the client-facing takeaway with the practitioner action item in each case.

The CLARITY Act is the most serious attempt yet to give crypto a proper legal home in the United States. It is not perfect — the stablecoin-interest fight alone could derail it, and the DeFi carve-out is likely to be the source of the next generation of enforcement disputes — but the political momentum is real, and the administration is pushing hard. For holders, the most actionable near-term item is the crypto wash-sale window, which may not survive the bill. For practitioners, the work to do now is classification analysis, 1099-DA reporting review, and a careful read of the DeFi carve-out language as it evolves. Waiting for the final text is not a strategy.

We continue to monitor these legal developments and provide strategies and analysis – follow us on LinkedIn here.

For further information on this topic, please reach out to Filip Rams at frams@smgglaw.com or Michael Nicolella at mnicolella@smgglaw.com.

©2026 Strassburger McKenna Gutnick & Gefsky | All Rights Reserved | Attorney Advertising | Disclaimer | Sitemap